Mobile

Mobile PC

PC

Full-Cycle

Full-Cycle Co-Development

Co-Development Outstaffing

Outstaffing

-

Game Development

Game Development

Mar 30th, 2026

Mar 30th, 2026- Share:

Table of Contents

- The UAE Gaming Market

- TL;DR — Key Takeaways

- The Growth of the UAE Gaming Industry

- What Is Interactive Game Development?

- Why Abu Dhabi Is Emerging as a Hub of Interactive Game Development

- Key Interactive Gaming Trends in the UAE for 2026

- Opportunities for Game Developers in the UAE

- Challenges in the UAE’s Interactive Gaming Market

- The Future of Interactive Gaming in the UAE

- Conclusion

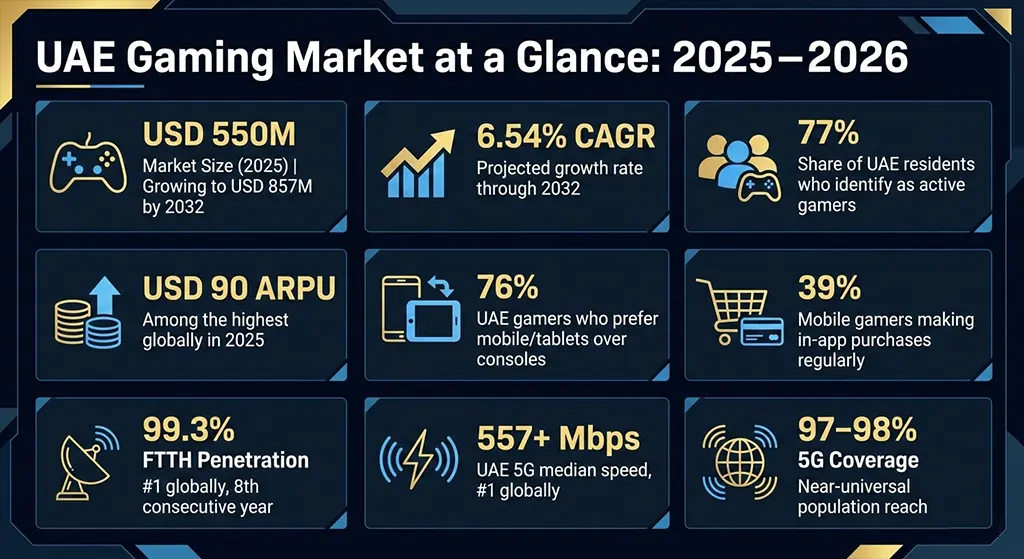

A decade ago, the United Arab Emirates was primarily a consumer of global gaming content. Today, it is systematically engineering its transformation into one of the world’s leading interactive game development hubs. With a gaming market valued at approximately USD 550 million in 2025 and projected to reach USD 857 million by 2032, the UAE is not simply following global trends — it is actively setting them.

What is driving this shift? A convergence of best-in-class connectivity, progressive government policy, and surging consumer demand for immersive interactive experiences has positioned the UAE at the frontier of game development in the Middle East, Africa, and South Asia (MEASA) region. For studios, investors, and technology partners, the opportunity window is wide open — and narrowing fast.

The UAE Gaming Market

The UAE gaming market is undergoing a structural transformation. Historically reliant on international titles and platform providers, the country has spent the past several years laying the groundwork for domestic and regionally-driven game production. The results are becoming visible: government-backed investment programs, emerging homegrown studios, accelerating infrastructure deployment, and a growing ecosystem of developers, publishers, and technology partners all converging around the UAE as a regional production base.

This article examines the market forces, emerging technologies, and strategic opportunities shaping interactive game development in the UAE through 2026. Market insights and key trends, such as technological advancements and demographic shifts, are driving the UAE gaming market, fueled by government initiatives supporting game development and digital content creation. It is written for studios evaluating market entry, investors assessing sector fundamentals, and businesses seeking co-development or outsourcing partnerships in this rapidly maturing region.

A tech-savvy population in the UAE, with high digital literacy and rapid adoption of new gaming technologies, is a key factor fueling growth and innovation in the sector.

The competitive landscape is defined by the presence of key players—leading game development companies and innovative startups—who are shaping the UAE gaming industry through strategic investments, partnerships, and cutting-edge projects. Their contributions are pivotal in establishing the UAE as a major hub for interactive game development in the region.

TL;DR — Key Takeaways

- The UAE gaming market is projected to grow from USD 586 million in 2026 to USD 857 million by 2032, at a CAGR of 6.54%.

- 77% of UAE residents already identify as active gamers — this is not an emerging market, it is an accelerating one.

- Mobile gaming dominates with approximately 75% device-share; online platforms account for ~90% of gaming activity.

- The UAE leads globally in 5G speeds (median 557+ Mbps) and FTTH penetration (99.3%), making it ideal for cloud- and mobile-first game development.

- The Dubai Program for Gaming 2033 (DPG33) targets 30,000 new jobs and a USD 1 billion contribution to GDP from the gaming sector.

- The GCGRA, established in September 2023 as the UAE’s first federal gaming regulator, provides the licensing and content framework, actively attracting international investment.

- AI, AR/VR, blockchain (Web3), and phygital gaming are the four technology vectors reshaping how games are built and consumed in the region.

- Cultural localization — particularly Arabic-fir+st content strategies — is a key differentiator for studios succeeding in the UAE market.

- Opportunities in LiveOps, co-development, educational games, and esports infrastructure are particularly strong heading into 2026.

The Growth of the UAE Gaming Industry

The UAE gaming industry has experienced what market analysts describe as an inflection point. According to MarkNtel Advisors, the market was valued at USD 550 million in 2025 and is forecast to reach USD 857 million by 2032, expanding at a CAGR of 6.54% during the forecast period. The market reportedly grew from USD 484 million in 2023 to over USD 1 billion in 2024 by some measures, with the UAE boasting one of the highest Average Revenue Per User (ARPU) rates globally, estimated at USD 90 in 2025.

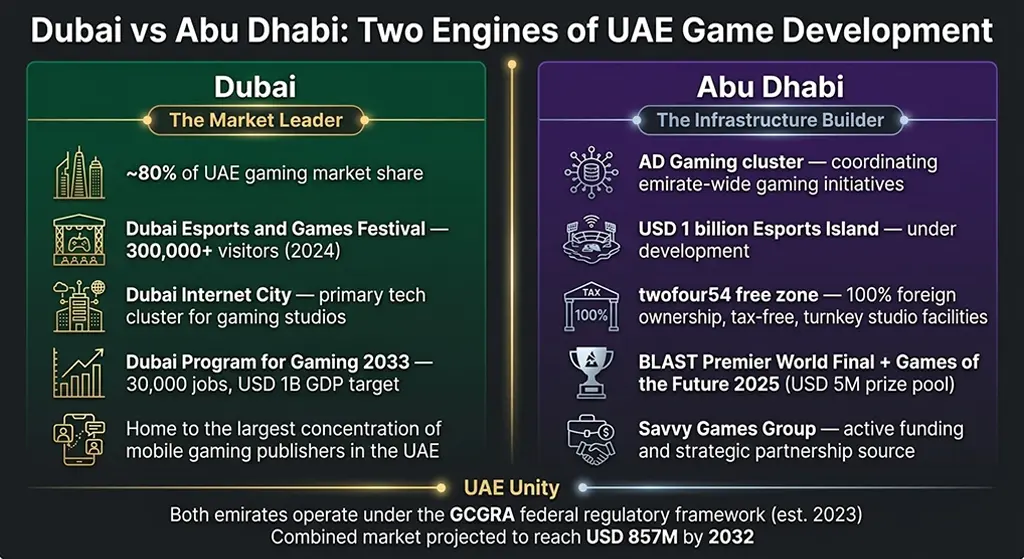

Dubai holds approximately 80% of the national gaming market share, making it the undisputed center of gravity for the UAE gaming ecosystem. The 19–35 age demographic accounts for roughly 62% of active players — a cohort that is digitally native, high-spending, and deeply engaged with both mobile and competitive gaming formats.

Critically, the UAE’s digital infrastructure underpins this growth in ways that few other markets can replicate — and for game developers, the numbers tell the story directly:

| Infrastructure Metric | UAE Standing | Relevance for Game Developers |

| FTTH Penetration | 99.3% — #1 globally (8th consecutive year) | Ultra-low latency for competitive multiplayer and cloud platforms |

| 5G Speed | 557+ Mbps median download — #1 globally | Enables cloud-native and high-fidelity mobile game streaming |

| 5G Population Coverage | ~97–98% | Near-universal access to low-latency mobile gaming |

| Mobile Subscriptions | ~21.1 million in a population of ~10 million (~200% penetration) | Massive addressable market for mobile-first titles |

| Active Fiber Network | 14.5 million km, connecting 2.88 million homes | Stable backbone for live-service and online multiplayer games |

With robust infrastructure, mobile dominates UAE gaming—76% prefer smartphones/tablets over consoles, driving 72-80% of revenue through high ARPU and near-universal access.

The UAE’s position as a regional technology and innovation hub — anchored in broader national strategies like UAE Vision 2031 and the National Innovation Strategy — has created an environment in which the gaming sector benefits from cross-sectoral investment in AI, cloud computing, and digital infrastructure. The popular video games in the UAE span mobile action titles, battle royale formats, and sports simulations, reflecting a consumer base that skews toward competitive, socially-driven experiences.

What Is Interactive Game Development?

Interactive game development refers to the design, engineering, and production of games that prioritize player agency, real-time responsiveness, and immersive engagement. Unlike passive media consumption, interactive games place the player at the center of a dynamic system — one that responds to their decisions, adapts to their behavior, and increasingly, connects them with other players globally.

In the contemporary context, interactive game development encompasses a broad range of technologies and formats, including the integration of immersive technologies such as AI, Web3, and other digital innovations. These technologies are playing a key role in enhancing the UAE’s gaming ecosystem, attracting international studios, and aligning gaming with the broader digital economy and innovation agendas:

- AR/VR Gaming — Creates spatial experiences that blur physical and digital boundaries. Key UAE venues already driving demand include VR Park Dubai (one of the largest VR entertainment venues globally), Yas Island theme park attractions in Abu Dhabi, Innovation City in Ras Al Khaimah, and AR city tours layered over cultural heritage sites

- AI-Driven Gameplay — Generates adaptive narratives, intelligent NPCs, and personalized difficulty curves

- Multiplayer & Social Experiences — From MMOs to competitive esports, transform games into networked social spaces

- Cloud Gaming — Delivers high-performance experiences without dedicated hardware; platforms like GeForce NOW, Blacknut, and Etisalat’s Arena Pro (bundling 100+ titles for subscribers) are already active in the UAE

- Gamified Enterprise Experiences — Deploys game mechanics in healthcare, education, and retail for training, engagement, and marketing

For the UAE, the relevance of interactive game development extends well beyond entertainment. The government’s recognition of gaming as an economic sector — one that intersects with tourism, digital media, education, and technology export — reflects a sophisticated understanding of how interactive media creates value across industries.

Why Abu Dhabi Is Emerging as a Hub of Interactive Game Development

While Dubai commands approximately 80% of the UAE’s interactive gaming market by revenue, Abu Dhabi is where much of the structural investment in interactive game development is being concentrated. Its combination of infrastructure, regulation, and long-term economic strategy positions it as an undisputed leader in shaping the region’s production capabilities — not just its consumer market.

Infrastructure that accelerates development at scale

- World-class digital infrastructure — high-speed connectivity, advanced data centers, and comprehensive fiber optic networks — creates ideal conditions for cloud gaming, mobile, and location-based immersive entertainment

- This digital backbone supports the full spectrum of interactive formats, from VR esports arenas to phygital event platforms

Progressive regulatory frameworks that actually work

- The AD Gaming platform offers funding incentives, business-friendly free zone environments, specialized training programs, and accelerator initiatives built specifically for game studios

- twofour54 free zone provides 100% foreign ownership, tax benefits, and turnkey studio facilities — removing typical barriers for international market entry

- The result is an ecosystem that thrives on structured institutional support rather than market speculation

Esports investment that builds global credibility

- Abu Dhabi invests in state-of-the-art venues and consistently hosts high-profile international tournaments

- Flagship events include the BLAST Premier World Final and the Games of the Future 2025 (USD 5 million prize pool)

- The planned USD 1 billion Esports Island further cements its position as the regional hub for competitive gaming with genuine global reach

An economic diversification strategy with gaming at its core

- Gaming aligns directly with Abu Dhabi’s broader push to diversify beyond oil — creating employment, driving technology adoption, and building digital entertainment export capability

- These investments contribute to the UAE’s ambition of becoming a global interactive media hub

For game developers, publishers, and investors evaluating where to establish a regional presence, Abu Dhabi represents not just current infrastructure — but the dynamic future of UAE interactive gaming.

Key Interactive Gaming Trends in the UAE for 2026

1. Mobile Dominance and the Mobile-First Development Mandate

Mobile gaming drives ~75% device-based activity in the UAE gaming market, and 72-80% of revenue, led by battle royale, action, sports, and hyper-casual genres optimized for short smartphone sessions. For studios, mobile-first development is foundational in this market.

Hyper-casual games have also surged in popularity, dominating download charts due to their broad appeal and simple mechanics. For studios and developers, this creates a clear strategic imperative: mobile-first architecture is not optional in the UAE market; it is foundational.

With over 21 million active mobile subscriptions in a population of approximately 10 million people — equating to nearly 200% mobile penetration — and 5G coverage reaching the overwhelming majority of the population, the UAE presents near-ideal conditions for mobile game app development company solutions targeting high-ARPU markets. Monetization is further accelerated by the UAE’s seamless digital payment infrastructure: digital wallets and online transaction platforms make in-game purchases and microtransactions easy and accessible, driving consistently higher in-app purchase conversion rates than in most comparable markets.

2. Growth of AR and VR Gaming Experiences

The UAE has made deliberate investments in immersive technology infrastructure, particularly in the context of tourism and entertainment. VR arcades, immersive entertainment venues, and location-based experiences have proliferated across Dubai and Abu Dhabi. VR Park Dubai — located in Dubai Mall and one of the largest VR entertainment venues globally — stands as a flagship example of the scale these investments have reached. The intersection of gaming and tourism is not incidental — it is strategic. Events like the Dubai Esports and Games Festival draw international visitors and create demand for on-site interactive gaming installations that blend physical attendance with digital participation.

For game development studios with AR/VR specializations, the UAE presents partnership opportunities with hospitality operators, tourism authorities, and event organizers seeking custom immersive experiences. The educational and training sector represents another high-growth vertical, with government-backed initiatives prioritizing AR/VR applications in vocational and corporate learning environments.

3. AI-Powered Game Personalization and Development Efficiency

Artificial intelligence is reshaping interactive game development in the UAE on two parallel tracks: as a player-facing feature and as a production efficiency tool. On the player side, AI is being deployed for procedural content generation, NPC behavioral intelligence, anti-cheat systems, and adaptive difficulty — all of which increase engagement without proportional increases in content production costs. On the production side, AI-assisted pipeline tools are reducing the time and cost required to generate assets, test builds, and localize content.

The UAE’s AI strategy, formalized through the UAE National Strategy for Artificial Intelligence 2031, provides a favorable policy environment for studios experimenting with AI-native game development workflows. Local and regional studios are increasingly integrating machine learning frameworks into their Unity and Unreal Engine pipelines — a trend that is expected to accelerate through 2026 and beyond.

4. Government Initiatives Supporting the Gaming Ecosystem

Perhaps the most distinctive aspect of the UAE’s gaming growth story is the degree to which it is government-enabled. The Dubai Program for Gaming 2033 (DPG33) is the most prominent initiative, targeting the creation of 30,000 new jobs and the addition of USD 1 billion to Dubai’s GDP from the gaming sector over the coming decade. The program provides structural support for startups, established studios, and international companies seeking to establish regional operations in Dubai.

The General Commercial Gaming Regulatory Authority (GCGRA)—established in September 2023—oversees licensing and player protection for commercial gaming, while TDRA manages digital infrastructure.

Government-backed innovation hubs and free zones provide concrete operational benefits for studios establishing a regional presence. Dubai Internet City and Abu Dhabi’s twofour54 free zone — which offers 100% foreign ownership, tax benefits, and turnkey studio facilities — are among the most active clusters. Savvy Games Group is also emerging as a strategic partner and funding source for startups and international publishers seeking to localize and expand across the UAE and broader MENA region.

5. The Phygital Gaming Revolution

The UAE is pioneering an approach to gaming that has been termed “phygital” — the deliberate integration of physical athletic performance with digital competition. Abu Dhabi’s USD 1 billion Esports Island initiative and its participation in the Games of the Future event exemplify this trend. Phygital gaming requires interactive game development capabilities that extend beyond traditional screen-based gameplay — encompassing sensor integration, real-time data processing, and hybrid physical-digital scoring systems.

This represents a category creation opportunity for forward-thinking studios. The demand for phygital experience design is currently underserved relative to demand, and the UAE’s investment in the infrastructure needed to host such events positions it as the natural venue for this emerging format to develop.

6. Rise of Esports and Competitive Gaming

The UAE esports ecosystem grows rapidly, with Dubai/Abu Dhabi as regional hubs and the UAE Esports Federation creating pro pathways. MENA esports revenues expand above 20% CAGR, while the UAE’s strategic location attracts global tournaments.

Key events anchoring this position include the Dubai Esports and Games Festival — which drew over 300,000 visitors in 2024 — the BLAST Premier World Final hosted in Abu Dhabi (one of CS2’s premier global tournaments), and the Games of the Future 2025 in Abu Dhabi, which offered a USD 5 million prize pool featuring competitions that merge physical and digital gameplay. International partnerships with global gaming organizations are further enhancing the ecosystem and attracting cross-border investment.

For game development studios, the esports trajectory has practical implications. Titles built for competitive play require specific engineering investments: skill-based matchmaking (MMR/ELO systems), anti-cheat infrastructure, spectator modes, replay systems, and tournament API endpoints. Studios with demonstrated expertise in these areas have a distinct advantage in the UAE market.

7. Blockchain, Web3, and Play-to-Earn Evolution

Dubai has positioned itself as a global hub for blockchain and digital asset innovation. This policy stance has created a permissive environment for Web3 gaming development, with local studios and international companies establishing operations to build blockchain-integrated game experiences. The market is moving away from early-stage play-to-earn models toward more sustainable approaches: true digital asset ownership, tokenized in-game economies, and NFT integration that enhances rather than overshadows gameplay.

The banned games in the UAE reflect ongoing regulatory sensitivities around certain content categories — a context that Web3 game developers must navigate carefully when designing token economies and in-game purchase systems for the regional market. Studios experienced in compliance-conscious economy design carry a meaningful structural advantage.

8. Cloud Gaming and 5G-Enabled Experiences

The UAE’s connectivity advantage — already detailed in the infrastructure table above — has a direct commercial consequence: cloud gaming here is not a workaround for weak hardware markets, it is a genuine premium delivery channel. Platforms like GeForce NOW, Blacknut, and Etisalat’s Arena Pro (bundling 100+ titles for subscribers) are already active, reaching players on mid-range mobile devices with PC-quality experiences. Integration with smart TVs and low-cost hardware is further expanding the addressable household base beyond dedicated gaming hardware owners.

For studios, this changes the design calculus. Games targeting the UAE market should be built with cloud-render compatibility in mind — optimised for short sessions averaging 20–40 minutes, graceful handling of variable network conditions, and cross-progression between mobile, PC, and console, even when rendering is offloaded remotely. Platform providers, telecom operators, and gaming companies in the UAE are actively seeking content partnerships that leverage this infrastructure for game distribution, live events, and streaming-based gameplay

Opportunities for Game Developers in the UAE

The UAE gaming market presents a multi-layered opportunity set for studios, publishers, and development service providers across engagement models and specializations. From LiveOps retainers to full-cycle production contracts, the breadth of demand means that companies offering end-to-end game development services have multiple entry points into the regional ecosystem. Critically, the UAE also functions as a gateway to the broader MENA region — representing over 400 million potential players — making it a high-leverage market entry point for studios with regional distribution ambitions. An often-overlooked demand signal: approximately 60% of new MENA gamers are women, a demographic shift that has meaningful implications for genre selection, UX design, and monetisation strategy.

| Opportunity | What It Means for Studios |

| Co-Development Demand | UAE studios need external partners to extend capacity and fill skill gaps. Game co-development teams that integrate seamlessly into existing pipelines are in active demand. |

| Outsourcing as a Scale Strategy | Publishers prefer specialist partners over building large in-house teams. Game development outsourcing services offering scalable, cross-platform execution are well-positioned. |

| LiveOps & Post-Launch Management | GaaS models extend a game’s commercial life well beyond launch. Studios with LiveOps capabilities — content drops, economy balancing, retention analytics — have strong recurring revenue potential. |

| Arabic Localization & Cultural Adaptation | Arabic-first strategies, Ramadan events, and local narratives drive measurable engagement lift. Localization depth is a client requirement, not a differentiator. |

| Game Art Outsourcing at Scale | Rising production values mean growing demand for game art outsourcing services — from 2D/3D modeling and concept art to UI/UX and VFX — without the overhead of full in-house art teams. |

| Educational & Serious Games | VR safety training, AR learning tools, and corporate simulations are active government and enterprise procurement priorities. |

| Esports Infrastructure & Tooling | Competitive gaming venues need tournament platforms, broadcast tools, analytics dashboards, and multiplayer architecture specialists. |

Challenges in the UAE’s Interactive Gaming Market

A balanced assessment of the UAE’s interactive gaming market requires acknowledgment of the structural and operational challenges that developers and investors must navigate.

| Challenge | Root Cause | What Studios Should Do |

| Cultural Localization Complexity | UAE audiences require Arabic-first content, region-specific aesthetics, and sensitivity to religious observances — not just translation | Invest in native Arabic QA, cultural consultants, and localization pipelines from pre-production |

| Regulatory Navigation | GCGRA, TDRA, emirate-level media authorities, and child digital safety rules create overlapping compliance requirements | Build compliance checkpoints into design and content pipelines from pre-production; retrofitting after development is costly |

| Talent Competition & Skill Gaps | The domestic supply of experienced developers and technical artists is limited relative to demand, driving wage inflation | Studios looking to hire game designers locally face a constrained market; partnering with established outsourcing studios is often the more reliable path |

| Studio Competition | Global names (Ubisoft Abu Dhabi) and funded local studios compete for the same clients, talent, and publisher relationships | Differentiate on a specific vertical — genre expertise, technology stack, or service model — rather than competing on breadth |

| Saudi Arabia / Regional Competition | Saudi Arabia’s Savvy Games Group brings multi-billion dollar acquisition and investment firepower; NEOM entertainment initiatives are creating an alternative MENA hub | Prioritise speed-to-market and strategic partnerships over purely organic growth; UAE-specific positioning is essential |

| Infrastructure ROI Risk | Large-scale AR/VR installations and esports arenas require sustained content pipelines and repeat-visit traffic to justify investment | Design projects with multi-purpose monetisation (tourism, corporate events, training) and robust live-ops content calendars from day one |

The Future of Interactive Gaming in the UAE

Looking ahead to 2026 and beyond, several converging dynamics will shape the trajectory of interactive game development in the UAE.

- AI-Native Production Pipelines — Generative AI is compressing asset creation, narrative generation, and QA automation timelines. Studios that build AI-native workflows now will carry structural cost and speed advantages into the next development cycle.

- Metaverse and Persistent World Experiences — The UAE’s smart city infrastructure and investment in digital-physical integration create a genuine operational environment for persistent virtual worlds. It remains one of the few markets where metaverse gaming applications have credible commercial conditions to mature.

- Cross-Platform as a Baseline, Not a Premium — As UAE audiences diversify across mobile, PC, console, and emerging form factors, the demand to hire a video game developer increasingly lists cross-platform capability as a non-negotiable. Studios with unified codebases and adaptive quality systems will have a clear edge.

- Smart City Entertainment Integration — Interactive gaming is expected to move beyond screens into public spaces, transit corridors, and commercial districts through AR overlays and location-based mechanics. The UAE’s urban infrastructure investment makes it a natural testing ground for this format.

- 6G on the Horizon — With a national 6G roadmap targeting deployment around 2030 and new spectrum bands (600 MHz and 6 GHz) rolling out in 2025–2026, the connectivity foundation for next-generation game experiences is already being laid.

- Regulatory Maturity Driving Investment — As the GCGRA’s licensing framework matures, institutional investor confidence in the UAE gaming sector is expected to grow, channeling more capital into domestic studio development, esports infrastructure, and co-production deals.

- Cross-Media IP Convergence — Games will increasingly link with streaming platforms, influencers, and linear TV. IP is expected to move fluidly between esports tournaments, mobile mini-games, VR attractions, educational applications, and broadcast entertainment — demanding development architectures that support multiple output formats from unified content pipelines.

For studios and investors monitoring the region, the interactive game development in the UAE trajectory represents one of the most compelling emerging market narratives in the global games industry.

Conclusion

The UAE has moved decisively from gaming consumer to gaming producer. The convergence of world-class 5G and fiber infrastructure, government-backed investment programs, a high-spending mobile-dominant audience, and progressive regulatory modernization has created conditions for the UAE’s interactive gaming market to scale rapidly and attract serious international participation.

For game development studios, the message is clear: the UAE is not a future opportunity — it is a present one. Whether through direct market entry, co-development partnerships with regional studios, or the delivery of specialized services in LiveOps, art production, or technical development, the demand signals are strong and the structural foundations are in place. Studios that establish credibility and relationships in the UAE market over the next 12–24 months will be well-positioned as the sector’s growth compounds through the decade.

As a video game development studio serving global clients across mobile, PC, console, and XR platforms, Juego Studios understands what it takes to build production-grade games in demanding, high-standard environments. The capabilities required to succeed in the UAE — localization depth, cross-platform delivery, LiveOps expertise, and co-development integration — align precisely with what defines a mature, mission-ready development partner.

Frequently Asked Questions

The UAE gaming market was valued at approximately USD 550 million in 2025, projected to reach USD 857 million by 2032, growing at a 6.54% CAGR according to MarkNtel Advisors.

Mobile action/adventure, battle royale, sports titles, and hyper casual games dominate the UAE gaming scene. Mobile titles are especially popular, with the average gamer in the UAE spending 20-40 minutes daily on mobile titles. Mobile platforms account for approximately 75% of device activity and 90% of total regional gaming revenue.

The Dubai Program for Gaming 2033 targets 30,000 jobs and USD 1 billion in GDP impact. The GameForward Accelerator, launched in 2026, focuses on developing commercially viable Emirati game studios.

High ARPU, global-leading 5G and fiber infrastructure, favorable free zone business regulation, and strong government investment make the UAE one of the most structurally attractive gaming markets globally. The country’s tech-savvy population drives rapid digital adoption and innovation, further fueling the growth of interactive game development in the UAE. Seamless and secure digital payments are prevalent, facilitating in-game purchases and monetization for both developers and players. Additionally, Dubai’s strategic initiatives and investments in the gaming sector provide a competitive edge, strengthening its leadership position and attracting industry players to the region.

Arabic-first content, Ramadan-themed events, and local narratives significantly improve player engagement. Cultural adaptation is a core production requirement — not an optional enhancement — for sustained UAE market success.

Related Posts

Scale Game Development Without Hiring: A Guide to Co-Development Partnership

In today’s game development, speed, quality and adaptability are key, but scaling your team can be a challenge and hiring full-time talent can be expensive. Co-development has become the go-to model for studios looking to scale their efforts without the overhead of a permanent headcount, adding specialized expertise at precisely the right time while leaving the core team lean and focused. This guide covers when co-development makes sense for your studio, how to structure it effectively, and what separates a partnership that scales you from one that just adds headcount.

![Best Game Development Companies in India [2026]: Reviewed & Compared](https://www.juegostudio.com/wp-content/uploads/2024/08/game-development-companies-india.jpg)

Best Game Development Companies in India [2026]: Reviewed & Compared

Finding the best game development companies in India has become less about availability and more about judgment. With studios offering everything from mobile games to complex multiplayer and immersive experiences, the real challenge is understanding who can consistently execute at a high level.

Best Game Engines for Game Development in 2026

Games have become increasingly sophisticated and complex over the years. Game developers need more than just a great idea to create an engaging and successful title – they also need powerful tools at their disposal.