Mobile

Mobile PC

PC

Full-Cycle

Full-Cycle Co-Development

Co-Development Outstaffing

Outstaffing

-

Gaming Industry

Gaming Industry

Mar 11th, 2026

Mar 11th, 2026- Share:

Table of Contents

Australia has one of the highest household gaming participation rates globally, with over 80% of households engaging in video games.

That’s not a typo. While the rest of the world was busy debating whether gaming was a passing fad, Australians quietly became one of the most digitally entertained populations on the planet. From retirees picking up puzzle games on their tablets to competitive teams grinding ranked matches in Melbourne’s esports arenas, gaming has embedded itself into the fabric of Australian everyday life in a way few industries ever manage to achieve.

And yet, for all its cultural prominence, the video game industry in Australia remains one of the most underappreciated economic stories of the past decade.

Why the Australian Gaming Market Deserves a Closer Look

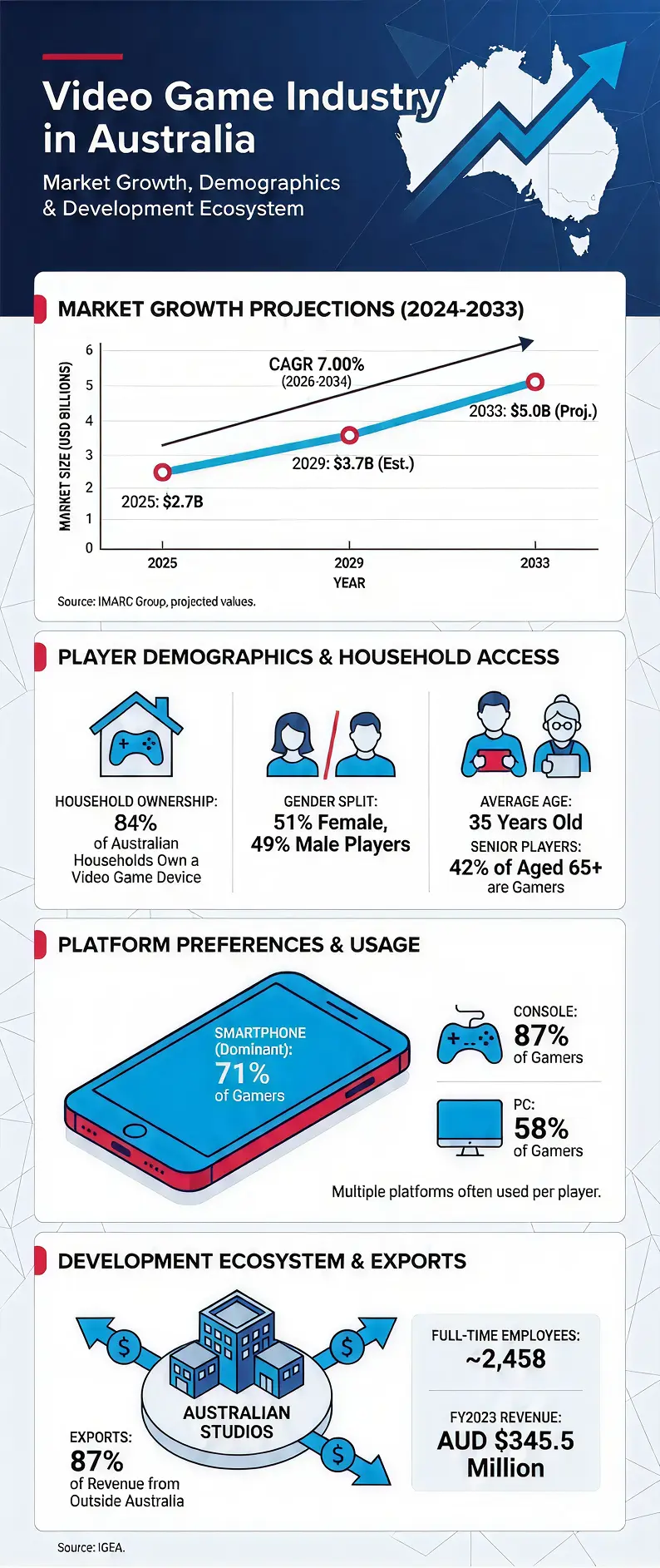

The video game industry in Australia is no longer just a consumer pastime — it is a significant and rapidly evolving economic sector. Worth an estimated USD 2.5 billion in 2024 and forecast to reach USD 4.9 billion by 2033, the local gaming ecosystem spans everything from independent game development studios and mobile publishers to esports organizations and government-funded creative programs.

What makes Australia particularly interesting is the convergence of high consumer engagement, a maturing local development scene, and increasing government recognition of gaming as both a cultural export and a tech sector driver. A 2022 Austrade report estimated that over 3,228 Australians were working in the video game industry — a number that has continued to climb as major studios expand their regional footprints and new independent developers emerge from university incubators and state-backed programs.

For investors, developers, and curious observers alike, understanding the video game industry in Australia means understanding one of the Asia-Pacific region’s most dynamic digital economies.

Current Market Size and Video Game Industry Statistics for Australia

By the Numbers

The figures surrounding the video game industry in Australia paint a picture of consistent, multi-front growth. Here is what recent data tells us:

The overall Australian gaming market was valued at USD 2.5 billion in 2024, according to IMARC Group reports, with projections to reach USD 4.9 billion by 2033 at a CAGR of 7.6%. Separate analyses like Grand View Research provide outlooks for the video game segment specifically (around USD 3-4 billion range through 2030), but broader digital entertainment inclusions are not standard in their gaming market definitions and lack the specific USD 12.6 billion (2024) or USD 31.8 billion (2030) figures at 16.5% CAGR cited.

What is consistent across reports is the direction: upward, and with confidence.

Some of the most telling video game industry statistics in Australia include:

- 84% of Australian households play video games, with high device ownership rates.

- Australian gamers average 35 years old, with women at 48% of players—near gender parity.

- 42% of those 65+ now game, driving accessibility-focused design.

- 60% use smartphones primarily, underscoring mobile dominance.

- Australia represents ~1-2% of global gaming revenue, outsized for its population.

- Valued at USD 15M in 2023, growing at 10.1% CAGR to 2028 per IMARC.

The Development Landscape

On the production side, the video game industry in Australia has matured significantly. The country is home to more than 130 active development studios, employing approximately 2,465 full-time professionals as of FY2024.

Victoria, New South Wales, and Queensland continue to dominate the studio landscape, supported by competitive state-level incentives and the Federal 30% Digital Games Tax Offset.

Screen Australia’s Games Production Fund and Emerging Gamemakers initiatives have played an important role in supporting independent teams and helping original Australian-made video games reach global audiences.

The export-driven nature of the sector is particularly notable: over 90% of Australian developer revenue now comes from overseas markets, reinforcing the country’s position as a globally integrated development hub.

Key Trends Shaping the Video Game Industry in Australia

1. Mobile Gaming Is the Undisputed Leader

Mobile was the largest revenue-generating segment in 2024, commanding a 56.98% share of the Australian gaming market. With 60% of the population already gaming on smartphones, the appetite for mobile titles shows no sign of slowing. Studios focusing on mobile game development services are finding a particularly receptive market in Australia, where commute times, outdoor lifestyles, and the ubiquity of high-speed internet create ideal conditions for short-session gaming.

2. AI Is Transforming Game Development

Artificial intelligence is no longer just a buzzword in game design — it is becoming a practical tool that is reshaping how games are built and experienced. AI is being used to generate dynamic game environments, personalize difficulty levels in real time, and automate testing pipelines that previously consumed enormous development hours. For Australia’s many small and mid-sized studios, AI integration is particularly valuable: it levels the playing field, allowing lean teams to produce content that rivals the output of larger international studios.

The KOCCA industry body has specifically highlighted AI adoption as a key factor that will strengthen the capabilities of smaller Australian studios in the years ahead.

3. Cloud Gaming and Subscription Services Are Gaining Traction

The expansion of Australia’s National Broadband Network (NBN) has dramatically improved internet access across urban and regional areas, making cloud gaming a viable option for a growing segment of the population. Services that allow players to stream high-quality games without expensive hardware are particularly attractive in a market where console penetration, while high, still leaves significant room for growth through alternative access models.

4. Esports Is Moving from Fringe to Mainstream

The Melbourne Esports Open drew over 17,000 attendees in 2019, and competitive gaming has only grown in visibility since. Local councils, educational institutions, and government bodies are increasingly sponsoring esports tournaments as community engagement tools and youth employment initiatives. The Australian Esports market’s projected 10.1% CAGR through 2028 reflects genuine momentum rather than speculative hype.

5. Shifting Monetization Models

Developers are rethinking how they generate revenue. Traditional one-time purchase models are giving way to a broader toolkit that includes in-game purchases, season passes, and live-service content. Understanding game monetization strategies is now as important for Australian developers as the quality of the game itself — particularly for mobile titles where free-to-play models dominate, and revenue depends on sustained player engagement over time.

6. A More Diverse Audience Driving New Game Concepts

With nearly half the gaming population being women, and significant engagement from players over 50, there is genuine market pressure on developers to diversify the kinds of experiences they create. Studios that are exploring fresh video game ideas — particularly those that emphasize narrative, accessibility, and social connection over pure reflex-based gameplay — are finding increasingly receptive audiences both domestically and internationally.

The Future of Australia's Video Game Development Industry

Opportunity at Scale

The future of Australia’s video game development industry is, by most credible measures, bright. Market projections consistently point to compounding growth across all major segments — mobile, console, PC, and online — through the early 2030s. The combination of strong consumer demand, improving development infrastructure, and growing government support creates a foundation that few comparable markets can match.

Key growth areas include:

- Serious and Applied Gaming: Educational gaming, healthcare applications, and training simulations represent an expanding frontier. With 65% of Australians having played games for educational purposes at some point, and growing institutional interest in gamified learning, this segment offers substantial runway.

- VR and AR Gaming: While still a small portion of the overall market (VR devices are in approximately 5% of gaming households), immersive technology adoption is accelerating. As headset prices fall and content libraries expand, Australian developers with early expertise in spatial computing will be well-positioned.

- International Collaboration and Export Growth: Australian studios are increasingly participating in international co-productions and publishing deals. The industry’s strong export orientation — with most developer revenue traditionally coming from overseas markets — means that growth in the global gaming market directly benefits Australian developers.

- Esports Infrastructure: Investment in dedicated esports venues, university esports programs, and broadcast partnerships is creating a more sustainable competitive gaming ecosystem that could generate meaningful employment and tourism in the years ahead.

Challenges That Cannot Be Ignored

A candid Australian video game industry report must acknowledge the headwinds alongside the tailwinds.

- Talent Acquisition and Retention: The industry employs over 3,500 professionals, but competition for skilled developers is fierce, both from domestic employers and international studios offering remote roles. Australia’s relatively high cost of living, particularly in Sydney and Melbourne, adds pressure to compensation expectations.

- Studio Consolidation: Post-pandemic, a number of smaller Australian studios have been acquired by or absorbed into larger international publishers. While this brings resources, it can also redirect creative decision-making offshore, reducing the distinctive character of locally developed content.

- Content Classification and Regulation: Australia has historically maintained one of the more restrictive content classification systems in the developed world. Titles involving certain themes or content levels have faced bans or required significant modification, which creates compliance complexity for both local developers and international publishers. The category of banned video games in Australia remains a live policy debate, particularly as the lines between interactive entertainment and other media continue to blur.

- Market Fragmentation: With mobile dominating revenue but console and PC commanding the most engaged player segments, developers must make difficult decisions about platform focus, particularly in a market where development resources are often constrained.

- Partnering with an experienced game development company that understands the specific regulatory landscape, platform preferences, and audience demographics of the Australian market can meaningfully reduce these risks for studios entering or expanding in the region.

You Can Also Checkout: Average Cost of Game Development in Australia

Conclusion

The video game industry in Australia is a mainstream, high-growth sector backed by near-universal consumer engagement, a diversifying player base, and increasing government investment. With the market forecast to nearly double by 2033, the opportunity for developers, investors, and publishers — including leading game development companies in Australia — operating in this space is substantial.

What the data makes clear is that Australia’s gaming story is still in its early chapters — and the next ones promise to be the most interesting yet.

Frequently Asked Questions

The Australian gaming market generated approximately AUD $3.8 billion (around USD $2.5 billion) in 2024. Industry forecasts suggest steady growth through 2030, driven by mobile expansion and digital distribution.

Mobile gaming is the largest revenue segment in Australia, accounting for over AUD $1.5 billion in 2024. While consoles remain highly popular, 81% of Australian households own at least one gaming device.

Yes. The Australian government supports the industry through initiatives such as the 30% Digital Games Tax Offset and funding programs administered by Screen Australia. These initiatives help independent studios scale production and compete globally.

Key challenges include talent shortages, studio consolidation by international publishers, content classification restrictions, and competitive pressure from global remote work opportunities.

The outlook is positive, with strong projected growth in mobile, esports, VR/AR, and applied gaming. Government support and export-oriented studios are expected to drive significant expansion through 2030.

Related Posts

How Game Porting Works: Process, Stages, and Cost Breakdown (2026 Guide)

How does game porting work? This is one of the most frequent questions game developers ask as they look to expand their reach and take advantage of the different platforms available today. The game porting process is an important part of how developers can leverage the different platforms for their game, allowing them to reach a […]

Cost of Game Development in Australia: Budget Planning for Indie and Studio Projects

This blog talks about what it costs to build a video game in Australia in 2026 — covering developer salaries, project-type budgets, phase-by-phase cost breakdowns, Australian tax incentives like the Digital Games Tax Offset (DGTO), hybrid outsourcing strategies, and common budget mistakes studios make.

Gaming Industry in Ireland: Market Size, Studios & Future Outlook

This blog talks about the gaming industry in Ireland — exploring its €600M+ market size, major studios and gaming companies in Ireland, the government’s Digital Games Tax Credit, structural challenges like developer pay and housing costs, and the outlook for the Irish game industry through 2027 and beyond.